Stakeholder Gold Corp. follows the World Resource Institute Greenhouse Gas Protocol (GHG Protocol) in reporting carbon emissions. In considering carbon emissions, we operate in local communities but reside in global communities. Mitigating our carbon footprint begins with understanding what that footprint is.

The Greenhouse Gas Protocol GHG Protocol is the leading global framework for measuring, managing and reporting Greenhouse Gas (GHG) emissions. For accounting purposes, emissions are categorized as Scope 1, 2 & 3 and calculated as follows:

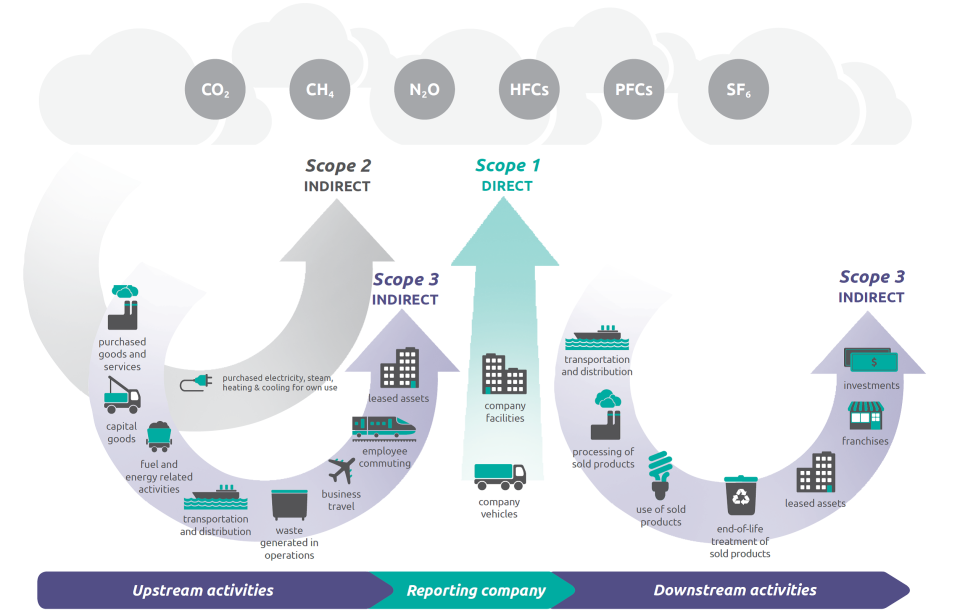

Scope 1 emissions are direct greenhouse (GHG) emissions that occur from sources that are controlled or owned by an organization (e.g., emissions associated with fuel combustion in boilers, furnaces, vehicles).

Scope 2 emissions are indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling. Although scope 2 emissions physically occur at the facility where they are generated, they are accounted for in an organization’s GHG inventory because they are a result of the organization’s energy use.

Scope 1 and Scope 2 Inventory Guidance

Source: EPA, United States Environmental Protection Agency

Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly impacts in its value chain. Scope 3 emissions include all sources not within an organization’s scope 1 and 2 boundary. The scope 3 emissions for one organization are the scope 1 and 2 emissions of another organization. Scope 3 emissions, also referred to as value chain emissions, often represent the majority of an organization’s total GHG emissions. Scope 3 emission sources include emissions both upstream and downstream of the organization’s activities.

Source: EPA, United States Environmental Protection Agency

Overview of GHG Protocol scopes and emissions across the value chain

Source: WRI/WBCSD Corporate Value Chain (Scope 3) Accounting and Reporting Standard

According to the GHG Protocol, all organizations should quantify scope 1 and 2 emissions when reporting and disclosing GHG emissions, while scope 3 emissions quantification is not required. However, more organizations are reaching into their value chain to understand the full GHG impact of their operations. In addition, because scope 3 emission sources may represent the majority of an organization’s GHG emissions, they often offer emissions reduction opportunities. Although these emissions are not under the organization’s control, the organization may be able to impact the activities that result in the emissions. The organization may also be able to influence its suppliers or choose which vendors to contract with based on their practices.

Ref: GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard